Written by Frode Skar, Finance Journalist.

Nvidia posts record fourth quarter and fiscal 2026 results as AI demand accelerates

Nvidia fourth quarter fiscal 2026 results set new benchmarks for revenue margins and cash returns

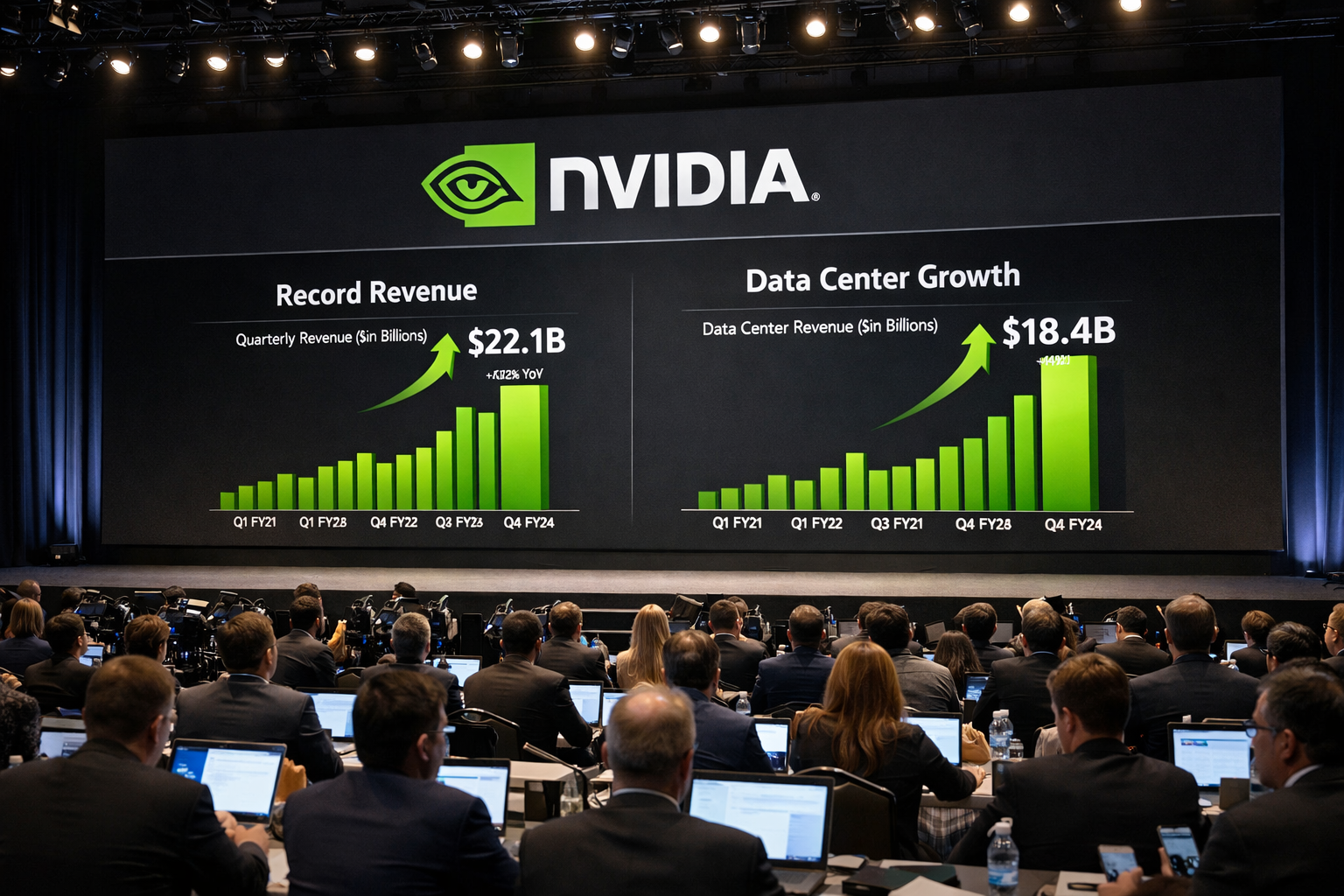

Nvidia delivered Nvidia fourth quarter fiscal 2026 results with record quarterly and full year revenue, reinforcing its position as the core supplier of compute for the global artificial intelligence build out. The company reported revenue of 68.1 billion dollars for the quarter ended January 25 2026, up 20 percent from the prior quarter and up 73 percent year over year. For fiscal 2026, Nvidia revenue reached 215.9 billion dollars, up 65 percent from the prior year.

The numbers confirm that AI infrastructure spending remains the dominant capital cycle in technology. Nvidia fourth quarter fiscal 2026 results also highlight a business model that is expanding at scale while maintaining unusually high profitability.

Gross margin for the quarter was 75.0 percent on a GAAP basis and 75.2 percent on a non GAAP basis. For fiscal 2026, gross margin was 71.1 percent GAAP and 71.3 percent non GAAP. Earnings per diluted share were 1.76 dollars GAAP and 1.62 dollars non GAAP for the quarter. For the full year, earnings per diluted share were 4.90 dollars GAAP and 4.77 dollars non GAAP.

Nvidia fourth quarter fiscal 2026 results are therefore not only about growth. They are also about margin structure, operational leverage and the durability of demand for inference and training.

Data Center revenue drives Nvidia fourth quarter fiscal 2026 results

Data Center revenue reached a record 62.3 billion dollars in the quarter, up 22 percent sequentially and up 75 percent year over year. For the full year, Data Center revenue climbed to 193.7 billion dollars, up 68 percent.

This dominance matters because it means Nvidia fourth quarter fiscal 2026 results are effectively a proxy for global AI capital expenditure. When Data Center growth accelerates at this scale, it is a signal that hyperscalers, enterprises and infrastructure providers are still expanding AI capacity aggressively.

The company framed the cycle as moving deeper into agentic AI, with inference becoming a decisive driver of compute demand. In practical terms, that points to a shift from periodic training surges toward continuous production workloads, where cost per token and total cost of ownership become central metrics.

Nvidia highlighted its Grace Blackwell platform with NVLink as a leader in inference economics and positioned the Vera Rubin roadmap as the next step in extending that advantage. For investors, the strategic message is clear: Nvidia is trying to defend its pricing power and platform relevance by anchoring the narrative on cost efficiency, not just peak performance.

Margins remain exceptional as expenses rise with scale

Nvidia gross margins remain extraordinarily high by semiconductor standards. However, fiscal year margins were lower than the prior year, which is notable given the rate of growth. In a business with this level of revenue, small changes in margin translate into large changes in profit dollars.

Operating expenses for the quarter were 6.794 billion dollars on a GAAP basis, up 16 percent from the previous quarter and up 45 percent from a year earlier. Nvidia is investing heavily across research and development, software ecosystems and platform level integrations. Nvidia fourth quarter fiscal 2026 results reflect a company expanding beyond chips into systems, networking and software infrastructure.

A critical reporting change also emerged. Beginning in the first quarter of fiscal 2027, Nvidia will include stock based compensation expense in its non GAAP financial measures. That shifts how investors should compare non GAAP results across periods. It can also reduce the perception that non GAAP metrics are stripping out a significant and recurring cost, encouraging more focus on free cash flow and underlying profitability.

Shareholder returns highlight financial strength

During fiscal 2026, Nvidia returned 41.1 billion dollars to shareholders through share repurchases and cash dividends. At the end of the fourth quarter, the company had 58.5 billion dollars remaining under its share repurchase authorization.

Nvidia will pay its next quarterly cash dividend of 0.01 dollars per share on April 1 2026 to shareholders of record on March 11 2026.

These numbers signal substantial balance sheet capacity. At the same time, investors should interpret buybacks in context. In technology firms, repurchases often serve both as capital return and as a mechanism to offset dilution from stock compensation. Nvidia fourth quarter fiscal 2026 results make that nuance more relevant given the shift to include stock based compensation in non GAAP reporting going forward.

Fiscal 2027 outlook and what is excluded

For the first quarter of fiscal 2027, Nvidia guided revenue of 78.0 billion dollars plus or minus 2 percent. The company expects GAAP and non GAAP gross margins of roughly 74.9 percent and 75.0 percent, respectively, plus or minus 50 basis points. GAAP operating expenses are expected to be about 7.7 billion dollars and non GAAP operating expenses around 7.5 billion dollars, inclusive of stock based compensation.

One line in the outlook stands out. Nvidia is not assuming any Data Center compute revenue from China in its guidance. That is significant because it frames near term expectations around demand in North America, Europe and other regions while acknowledging uncertainty around China exposure.

For investors, excluding China from the outlook can be interpreted as risk management. It reduces the chance of negative revisions tied to regulatory or geopolitical constraints, but it also means headline growth is being guided without that potential contributor.

Platform expansion and partnerships underpin demand

Nvidia used the results release to emphasize major platform developments and partnerships. The company unveiled the Rubin platform roadmap, describing a set of new chips targeting major reductions in inference token cost compared with Blackwell. Large cloud providers including AWS, Google Cloud, Microsoft Azure and Oracle Cloud Infrastructure are expected to be among the first to deploy Vera Rubin based instances.

The company also highlighted BlueField 4 as part of a new AI native storage approach aimed at inference context memory. Strategically, that suggests Nvidia is working to capture more value per data center build by extending beyond GPUs into networking and data movement, where bottlenecks increasingly define real world AI performance.

Nvidia also referenced a multiyear strategic partnership with Meta spanning on premises, cloud and AI infrastructure, including deployments of Nvidia CPUs, networking and millions of Blackwell and Rubin GPUs. The broader message is that Nvidia wants to be embedded as a platform supplier across the entire AI stack.

Other segments provide breadth but Data Center sets the pace

Gaming revenue was 3.7 billion dollars in the quarter, up 47 percent year over year but down 13 percent sequentially due to normal channel inventory behavior after a strong holiday season. Full year Gaming revenue was 16.0 billion dollars, up 41 percent.

Professional Visualization revenue was 1.3 billion dollars in the quarter, up 74 percent sequentially and up 159 percent year over year, driven by Blackwell demand. Full year revenue in the segment rose to 3.2 billion dollars.

Automotive revenue was 604 million dollars in the quarter, up 6 percent year over year. Full year Automotive and Robotics revenue rose 39 percent to a record 2.3 billion dollars.

These segments add diversification, but the key takeaway from Nvidia fourth quarter fiscal 2026 results remains the scale of Data Center growth.

Market implications after Nvidia fourth quarter fiscal 2026 results

For the market, Nvidia fourth quarter fiscal 2026 results raise the bar again. The core investor debate is no longer whether AI spending exists. It is about durability, cyclicality and pricing power.

Risks remain. Demand is concentrated among a small group of hyperscale buyers. If any major customer slows capital expenditures, growth rates could decelerate quickly. Competition also continues to intensify, and large cloud providers are building custom silicon for specific workloads.

Nvidia is attempting to counter those risks by shifting the narrative toward inference economics and agentic AI, which can be more continuous and consumption driven than training spikes.

The decision to exclude China from the Data Center outlook is also a reminder that geopolitical constraints are now part of the fundamental model.

Conclusion

Nvidia fourth quarter fiscal 2026 results delivered record revenue, record Data Center performance and substantial shareholder returns, confirming that the AI infrastructure cycle remains in expansion mode.

At the same time, the results introduce important forward looking considerations: a more transparent approach to non GAAP reporting, an outlook that excludes China Data Center revenue, and a strategy centered on lowering inference cost per token through new platform roadmaps.

Nvidia fourth quarter fiscal 2026 results are a strong signal of momentum. They also set expectations even higher, making execution and guidance credibility the decisive variables for the quarters ahead.